target: stock exchange system

Step 1 - Understand the Problem and Establish Design scope

functional requirements

- trade: only stocks

- order type: limit order

- normal trading hours

- basic function:

- place new limit orders

- cancel an order

- receive matched trades in real time

- view the real-time order book

- support at least tens of thousands of users trading at the same time.

- at least support 100 symbols

- trading volume: support billions of orders per day

- risk checks: like a user can only trade a maximum of 1 million shares of Apple stock in one day

non-functional requirements

- Availability: at least 99.99%.

- Fault tolerance: a fast recovery mechanism

- Latency: The round-trip latency should be at the millisecond level

- Security: account management and KYC and prevent DDoS

back-of-the-envelope estimation

- 100 symbols

- 1 billion orders a day

- 6.5 hours in total a day.

- QPS: 1 billion / 6.5 / 3600 = ~43,000

- Peak QPS: 5 * QPS = 215,000.

Step 2 - Propose High-Level Design and Get Buy-In

business knowledge 101

- broker: like Robinhood

- bid price: the highest price a buyer is willing to pay for a stock

- ask price: the lowest price a seller is willing to sell the stock

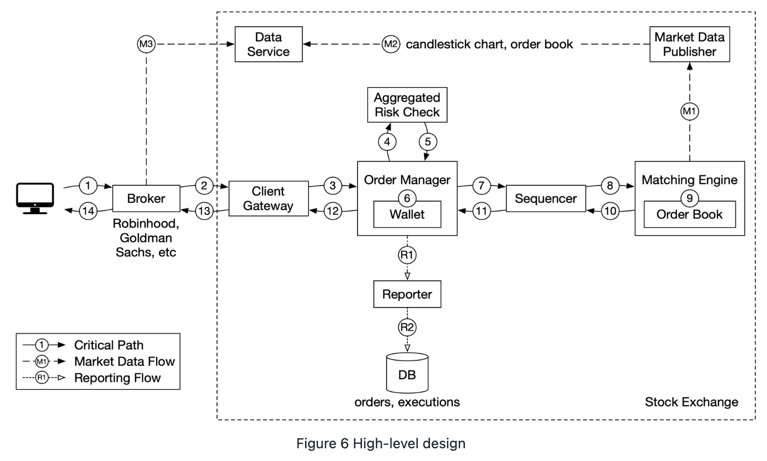

High level design

Step 3 - Design Deep Dive

- trading flow:

- matching engine

- sequencer

- order manager

- client gateway

- Market data flow

- Reporting flow

API Design

Data models

production, order, execution

order book

The following code snippet shows an implementation of the order book.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

class PriceLevel{

private Price limitPrice;

private long totalVolume;

private LinkedList<Order> orders;

}

class Book<Side> {

private Side side;

private Map<Price, PriceLevel> limitMap;

}

class OrderBook {

private Book<Buy> buyBook;

private Book<Sell> sellBook;

private PriceLevel bestBid;

private PriceLevel bestOffer;

private Map<OrderID, Order> orderMap;

}

比较核心的就是这个order book的设计。

- orders的数据结构设计为双向链表。维护一个Map<orderId, Order>的结构,当删除一个order 的时候就可以直接定位到order,然后在双向链表中进行删除就是O(1)的时间复杂度。

.png)